Half Year Results for the six months ended 30 September 2024

12 November 2024

Renewi plc (“Renewi”, the “Company” or, together with its subsidiaries, the “Group”) (LSE: RWI, AMS: RWI), the leading European waste-to-product business, announces its results for the six months ended 30 September 2024 (“HY25” or the “Period”).

Financial Highlights

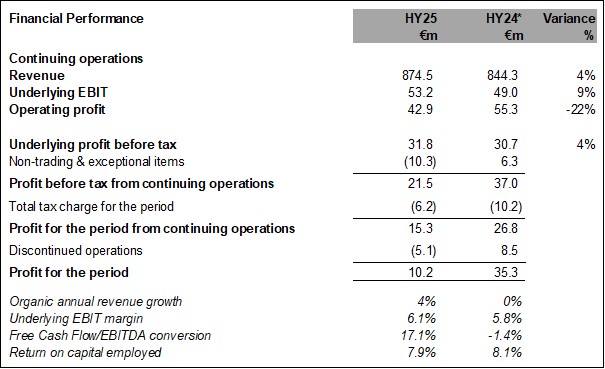

- Revenue from continuing operations up 4% to €874.5m (HY24: €844.3m), mainly driven by pricing in Commercial Waste and strong growth in Specialities

- Underlying EBIT from continuing operations up 9% to €53.2m (HY24: €49.0m), driven by successful turn-around in Mineralz & Water (“M&W”) and benefits from Group margin improvement programmes. Underlying EBIT margin increased to 6.1% from 5.8% last year

- Statutory profit after tax of €10.2m (HY24: €35.3m) due to non-cash impact of changes in discount rates for long-term provisions and the loss for the period from discontinued operations

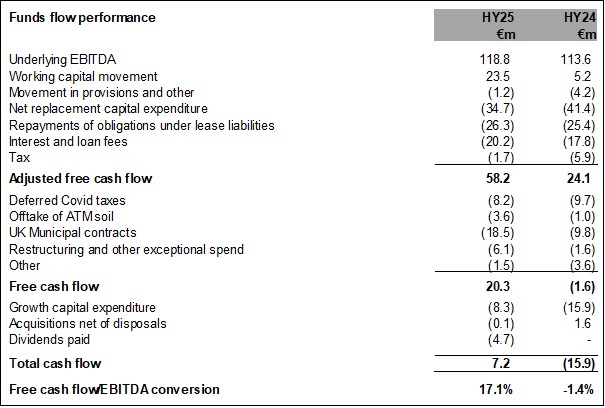

- Free cash flow improved to €20.3m including UK Municipal largely driven by underlying EBITDA growth and working capital improvements

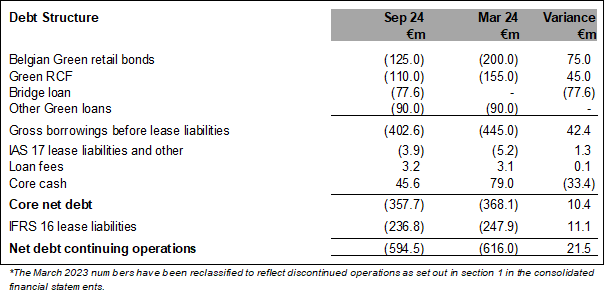

- Core net debt2 to EBITDAof 2.04x, down from 2.14x in March 2024, with core net debt reducing to €357.7m (March 2024: €368.1m). Following the UK Municipal sale on 10 October 2024, proforma net debt would be 2.85x. The Group continues to expect to deleverage by 0.4-0.5x per annum to 2x.

Strategic & Operational Highlights

- Portfolio restructuring executed: Fundamentally improved risk and cash generation profile. UK Municipal divestment completed on 10 October 2024, which will improve margins and free cashflow generation, and the M&W turn-around is on schedule realising double digit underlying EBIT margin

- Successful cost and efficiency measures: Reduced SG&A costs by €15M in FY24 and further incremental savings identified. Measures are being implemented to simplify our organisational structure, standardise and digitise our operations to drive efficiency, asset utilisation and customer satisfaction

- Organic growth: 4% revenue growth achieved driven by pricing in Commercial Waste and strong growth in Specialities despite a challenging market backdrop

- Commercial Waste: Realised 3% revenue growth in Commercial Waste despite continuing subdued volumes across certain market segments, reflecting the economic backdrop.

- Inbound price increases were implemented to offset additional handling cost of inbound waste due to previously outlined incinerator capacity issues

- Mineralz & Water: Strong performance, resulting in double digit underlying EBIT margins driven by higher year on year volume in soil and water treatment activities as well as lower utility costs and secondary building materials gaining momentum

- Specialities: Continued strong performance, with revenues increasing 19% and underlying EBIT growing 10%, benefiting from previous operational enhancements, pricing and strong volume intake at Coolrec

- Recyclate prices: Generally stable in the Period, with paper price increases and wood prices decreasing

- Recycling rate from continuing operations:Improved slightly over the Period to 66.2% (63.8% including UK Municipal) from 65.4% at FY24 (63.2% including UK Municipal).

Outlook

- Expectations for FY25 underlying EBIT from continuing operations unchanged

- FY25 dividend to be proposed after full year results in line with dividend policy

- Medium-term targets of high single digit underlying EBIT margins, Free Cash Flow/EBITDA conversion >40%, ROCE of >15% and >5% organic revenue growth are unchanged and on track.

Strengthened platform capable of accelerating strategic delivery

During the Period we have reached an important milestone in the transformation of the Group, as we are demonstrating delivery across the key enablers of our longer term strategic objectives:

- Structurally underperforming business units now exited or remediated;

- Ongoing net margin enhancement programmes embedded in the businesses; and Return to free cash flow generation.

Our strengthened platform supports the commitments made at the 2023 Capital Markets Day.

Portfolio optimisation

On 10 October 2024, shortly after the Period end, Renewi completed the sale of its UK Municipal activities to Biffa. The completion of this divestment de-risks Renewi's balance sheet and immediately improves both cash flow and underlying EBIT margin.

The focus on producing secondary building materials has paid off and resulted in strong financial performance of the M&W division realising an underlying EBIT of €8.8 million, a 5x increase versus last year.

Stronger platform

The Group launched and completed a cost-cutting programme in FY24 to streamline staff functions and reduce overhead costs, which is now generating annual SG&A savings of €15 million. Further initiatives have been launched and are to be implemented during the second half of FY25, focusing on building logistics, processing and engineering capabilities as well as standardisation in preparation for the Future Fit digitisation programme.

Renewi is committed to creating a more efficient operating model. To this end, Renewi has conducted initial site reviews, categorising locations into Processing and Logistics sites. Over the period, the Company has closed low-yielding sites, including Tisselt and Mijdrecht, and streamlined operations by reducing its fleet of trucks by approximately 50 vehicles or 3.2% of our total fleet. The Company is also making significant strides in improving working capital management, particularly in data cleaning, unbilled revenue, and accounts receivable, resulting in a €47 million trade receivables improvement versus March 2024. Initial steps towards working capital management standardisation and process enhancement have been initiated, which will be embedded in the subsequent digitisation programme.

Organic Growth

The Group launched a refreshed commercial strategy with a clear focus on specific sectors and segment requirements, as well as circular materials to ensure alignment of inbound and outbound commercial efforts. This approach allows us to offer better recycling solutions for our customers within strategic sectors and secure end-to-end profitability by aligning attractive inbound and outbound streams. Against the backdrop of growing momentum around CSRD and the energy transition, Renewi has started projects through partnerships in the area of chemical recycling of soft plastics, alternative fuels and circular products for the cement industry. Renewi is the first in the sector to offer customers a CSRD product based on third-party validated calculations for reporting along with related consulting services. This offering was launched in the Netherlands in early November and will be rolled out in Belgium over the next 12 months.

Otto de Bont, Chief Executive Officer, said:

Our half year results show tangible progress on our commitment to build a strong platform.

The successful divestment of UK Municipal on 10 October 2024 and the strong performance of M&W, supported by strategic investments and actions over the last two years, have allowed us to move beyond our legacy challenges, positioning us for future growth.

We have made significant progress in strengthening our business. The completion of our SG&A efficiency program is generating annual savings of €15 million. Ongoing initiatives are on track to standardise and digitise our operations, further enhancing our competitive edge and the strength of our growth platform.

Our pricing strategies for inbound services coupled with generally stable outbound recyclate prices have partially mitigated the impact of the slightly lower volumes due to subdued economic and industrial activity. Organic growth drivers include the successful launch of our customer CSRD reporting tool in The Netherlands, upgrades in our M&W operations with a new jetty commissioned in early November increasing degasification capacity, and customer wins underlining our material-focused sales strategy such as the partnership with VeenIX and Rijkswaterstaat for construction material recycling.

Virtual presentation

Renewi will host a virtual analyst presentation today at 10:30am CET if you would like to join the presentation, please sign-up here.

Today’s presentation will also be available on the website once the webcast has concluded.

HY25 Results

The underlying figures above are reconciled to statutory measures in notes 3 and 19 in the consolidated interim financial statements. * The FY24 numbers have been reclassified to reflect discontinued operations as set out in note 2 in the consolidated interim financial statements.

All numbers above contain both continued and discontinued operations. Free cash flow conversion is free cash flow as a percentage of underlying EBITDA. The non-IFRS measures above are reconciled to statutory measures in note 19 in the consolidated interim financial statements.